Introduction

Paying off debt is like a long, difficult marathon run. You have communicated to your creditors, paid off your debt, and are now free of it. But even after all of it is settled, your finances aren’t yet stable for the future.

You may also have outstanding things like amounts to pay, charges, tax demands, or negative credit entries. If not dealt with properly, outstanding things can cause confusion, distress, and even further debt trouble.

In this piece, we are going to discuss what residuals are after a debt settlement, how to handle them responsibly, and how to recover a sense of value and money management for the future.

1. Comprehending Debt Settlement Remains

Residual debt is a term used for money owed, penalties, etc., that remain even if your primary settlement payment is made.

These residuals can include:

- Small fractions of balances or accrued interest

- Fees and penalties are added before settlement and cleared

- Taxable income for debt released

- Adverse credit report marks

- Emotional and budgetary recovery activities (budget reconstruction, planning, etc.)

In a nutshell, paying off your debt does not necessarily mean everything vanishes overnight. Traces remain, and doing it right guarantees long-term success.

2. Why Residuals After Settlement Are Important

Even after a successful settlement, residuals are possible for some reasons:

- Timing gaps: The creditor charges tiny interest or fees until they finally shut down the account.

- Clerical mistakes: Misapplication of payment or failure to record appropriately through the system.

- Third-party transfers: Your records might not reflect this if your debt was transferred to a new collector.

- Related unpaid expenses: Attorney expenses, collector expenses, or settlement firm expenses.

- Tax debt: Taxable income can be considered for forgiven debt according to IRS requirements.

Being aware of those things assists in maintaining a keen eye on your accounts after settlement occurs.

3. Confirm Your Account is Closed for Business

The first thing to be done after settling a settlement is verification of the closure of your account.

You may achieve it by:

- Demand for a “paid in full” or “settled in full” statement by the creditor.

- Verifying your credit report between 30–60 days to ensure your bill appears as $0.

- Calling customer service/collections agency to find out if it’s shut down.

Unless it’s confirmed formally, the report might still seem active, and you may end up getting future notices of collections erroneously.

4. Processing of Remaining Amounts after Clearance

Once in a while, after settling, a notice for a few dollars or built-up interest will arrive and state that they are still owed money. Here’s how to deal with it:

- Don’t ignore it. Even small remaining balances can hurt your credit if they’re forwarded to a collections service.

- Call your creditor immediately and demand a statement of your account.

- Check for accuracy. If it’s a typing error, ask for a written correction.

- Pay minor amounts owed on time to complete the closure process.

e.g.

If your settled amount was $5,000 and a $25 fee was added for timeliness, being paid off guarantees no future problems.

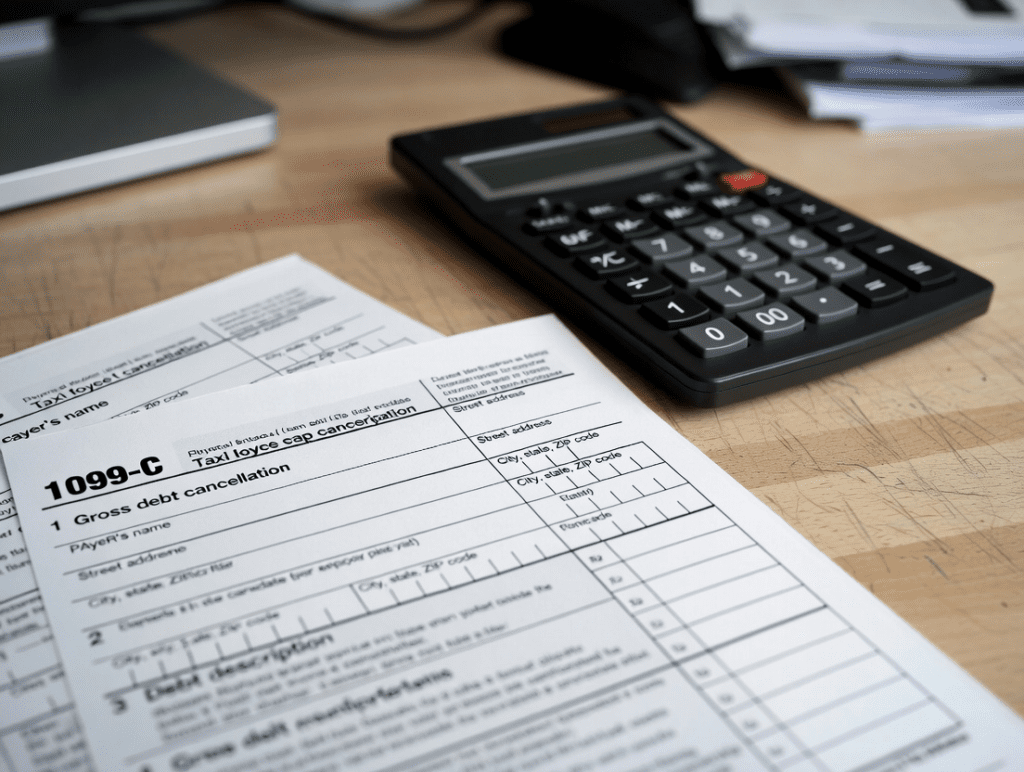

5. Tax Aspects of Discharged Debt

One of the largest “remainders” left following the settlement of debt is tax liability.

How It Works:

If a creditor discharges some of your debt, it counts as “income” to the IRS.

In case of forgiveness of $10,000, a Form 1099-C (Cancellation of Debt Income) might be sent your way next tax year.

What You Can Do:

- You report it on your tax form as income.

- If you are qualified as insolvent (your debt exceeded your assets), you are qualified for exclusion under IRS Form 982 to decrease or erase your tax liability.

- Always consult a tax professional to avoid mistakes.

Not correcting for it may result in penalties or a tax bill down the road.

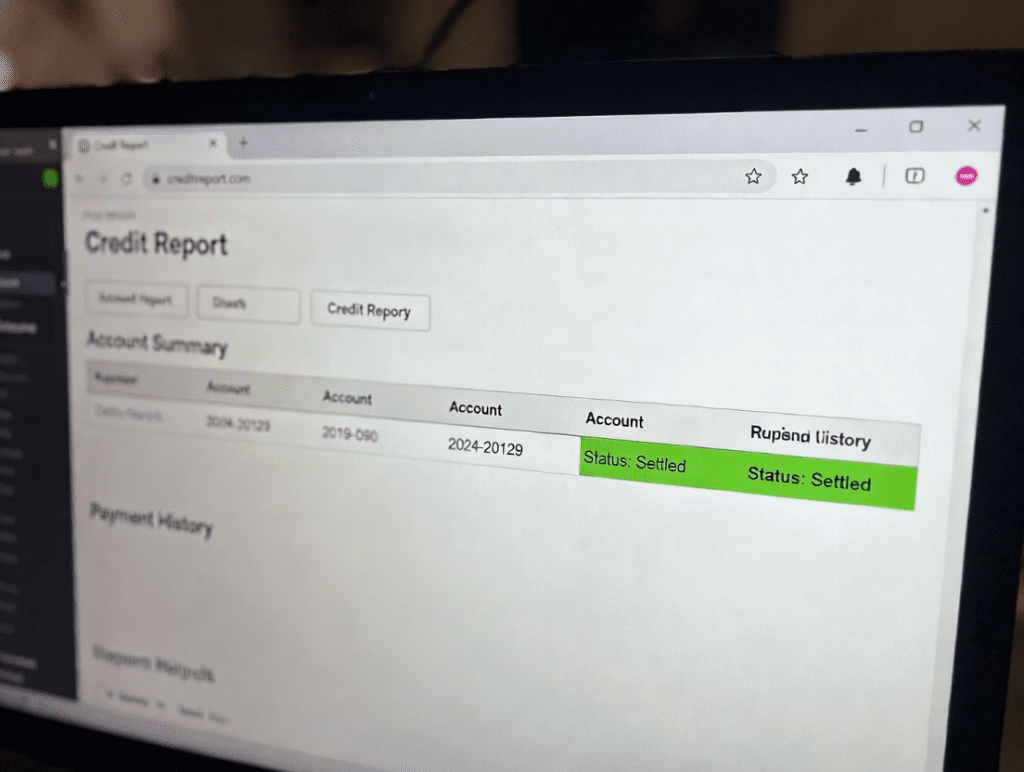

6. Following Your Credit Report After Settlement

Credit settlement impacts your record, yet controlling it helps prevent future harm.

That’s what to examine:

- The report should state “Settled” or “Paid – Settled for less than full.”

- The total should be $0.

- The creditor’s name should not be a repetition (same).

- The record cannot resurface again as “charged-off” or “in collections.”

If you find mistakes:

- Complain to Experian, Equifax, and Trans Union.

- Please attach your settlement letter and receipt of payment.

- Ask for correction within 30 days.

Proper follow-up avoids damage from erroneous reports.

7. Rebuilding Credit After a Settlement

Repaying debt, the next process is to repair your finances.

Credit recovery is never a one-time event, but regular efforts pay real dividends.

Rebuilding Process Steps:

- Pay all current accounts on the due date.

- Maintain credit card utilisation below 30% of their capacities.

- Get a loan to build credit or a secured credit card.

- Do not apply for several new accounts simultaneously.

- Check your credit reports several times a year.

In 12–24 months, your score could radically change if you remain consistent.

8. Dealing with Collection Mistakes After Settlement

Sometimes, even after settling the pay, a collector will attempt to contact you often due to poor recordkeeping.

If it occurs:

- Do not panic.

- Give a copy of your settlement agreement and your payment receipt to them.

- Ask for verification of debt under the Fair Debt Collection Practices Act (FDCPA).

- Visit the website of the CFPB if they persist in calling you illegally. You are entirely legally protected when your debt is actually paid and settled formally.

9. Dealing With Remaining Payments or Settlement Company Fees

If you dealt with a debt settlement firm, review for:

- Any other administrative fees owed by you.

- Whether all creditor payments were made.

- Your trust/escrow account for settlement is vacant and closed.

You should always receive written confirmation of your settlement company indicating:

- “All your creditor payments have been settled, and there’s nothing left outstanding for your account.”

This guarantees complete financial closure.

10. Emotional & Mental Residuals After Settlement

Settling debt isn’t merely a money issue; it’s psychological. A lot of individuals experience guilt, stress, or repercussions of future debt.

This is how to move ahead boldly:

- Celebrate your success: You responsibly paid off your loans.

- Do not live on past failures. Look to development.

- Develop healthy money habits: Budget, save, and spend money on record.

- Seek counselling or money coaching if money is on your mind.

Your mental health is of no less importance than your financial health at settlement.

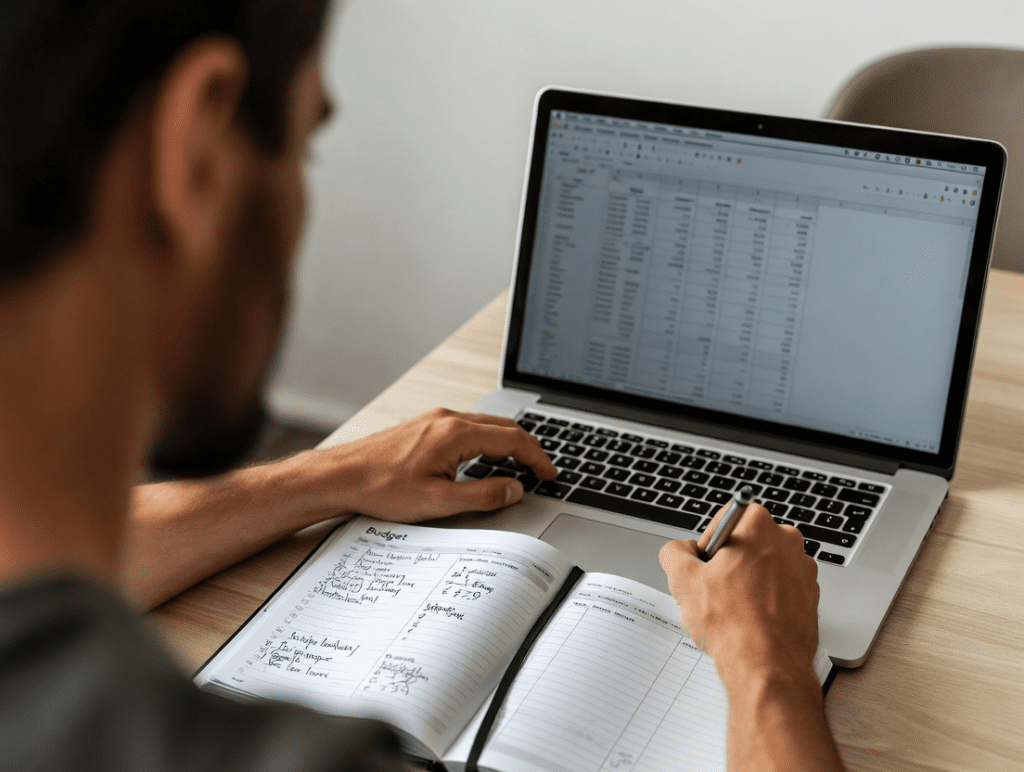

11. Developing a Post-Settlement Financial Plan

With your large bills paid off, it’s time to stabilise through a systematic approach.

Main Steps:

- Create a realistic monthly budget.

- Establish a minimum of 3–6 months’ expenses’ emergency funds.

- Begin planning for retirement or for investing.

- Minimise applications for credits.

- Track your progress using financial apps or spreadsheets.

Having a plan Avoid getting into debt again, and setting your finances on a secure path.

12. Handling Multiple Settled Accounts

If you have settled many debts, each of them might have its own residual tax statements, residual amounts, or misplaced reports.

Maintain a separate “Debt Resolution File” with:

- Copies of each settlement letter,

- Payment acknowledgements,

- Tax statements (1099-Cs), and

- Any correspondence by creditors.

This methodical approach spares you confusion or conflict later on.

13. Determining When “Residual Interest” Arises

Certain lenders, like credit card lenders, require residual interest earned between your prior statement and your pay date.

To handle it:

- Ask the lender if there is a remaining interest after the settlement clears.

- Ask for a final payoff statement setting a zero amount.

- Pay if invoiced later for a nominal fee, and request an acknowledgement by mail.

This helps to prevent sending the debt incorrectly back to collections.

14. Be Aware of Scams After Settlement

However, when your name appears on settlement lists, your settlement servicer can call and/or write letters falsely purporting to collect money owed by you.

Cover yourself with:

- Verifying the source before transferring money.

- Verifying whether your collector or creditor is registered with your state’s regulator.

- Having all of your pre-settlement documents on hand.

- Never disclose personal information to unknown dialers.

Once your account is settled, no reputable agency should need additional funds.

15. When to Seek Legal or Professional Advice

If you encounter difficulties such as:

- Ongoing collections activities,

- Tax confusion regarding cancelled debt, or

- Settlement firm malpractice

It’s better to inquire:

- A consumer protection attorney,

- A certified counsellor of credit, or

- A tax practitioner.

They can help you through lingering worries and advocate for your fiscal rights.

16. Changing Settlement into a New Beginning

Debt settlement, if conducted properly, is a turning point.

You’ve acted decisively, bargained responsibly, and it’s your turn to rebuild.

Do these steps next:

- Re-evaluate your goals financially.

- Develop a routine of savings.

- Learn about credit management for yourself.

- Celebrate your success responsibly.

Bankruptcy is not the end of your life; it’s the beginning of a financially sound, debt-free life.

Conclusion

Payoff of your debt is a great achievement, but understanding how to deal with residuals after payoff guarantees your relief is complete and ongoing.

By verifying account closings, covering tiny remaining balances, checking your credit, and getting a head start on taxes, you’ll shield yourself from future problems.

Make use of this aspect to establish a stable base of finances: keep savings, handle credit intelligently, and continually expand your personal finances knowledge.

Being debt-free isn’t something you start after settlement; it starts there.

FAQs

[…] you are engaged by a debt settlement organization, it is even riskier to skip payments. Debt settlement organizations accept funds towards a […]

[…] debt settlement agreement is a written, enforceable contract between a creditor/collection agent (your creditor) and a […]

[…] Learn more about handling debt after settlement. […]