Overview

When you get behind on payments on your debts, either bills or loans, not terribly surprisingly, not only will you be contacted by the debt to which you owe money, but by collection agencies seeking to collect the money that you owe. Notably, recognize that while creditors do hold a legal right to seek the money collections that you owe to them, you, being a debtor, hold important legal rights that have been codified to keep you from being harassed, treated unfairly, or otherwise abused by individuals to whom you owe money. Staying well-informed about your legal rights as a debtor is utterly imperative to responsibly handling debt and to keep you safeguarded against any unlawful means of collections that may be made against you.

The piece below holds a detailed explanation of debtor rights, federal law, common breaches by creditors, negotiating advice, and safeguarding oneself while facing financial hardships.

Understanding the Details of the Debtor-Creditor Relationship

Who is a Debtor?

A debtor can essentially be any individual or business entity that is faced with the situation of having to owe money to another entity, known more widely as the creditor. Debts can be derived through any source, such as but not limited to credit cards, personal loans, medical bills, mortgages on property, or even defaulting on utility payments.

Who Is a Creditor?

The creditor refers to a bank, financial institution, or company lending money by extending credit to the debtor. When payments default, the creditors can try to collect directly or through external collection agencies.

Relevance of Debtor Rights

The absence of effective legal protection for debtors would make them vulnerable to any kind of harassment, intimidation, and unfairness that could significantly impair their lives. That’s precisely why consumer protection law is supposed to exist; it works to achieve a reasonable balance between a debtor’s creditors’ rights to recover debts and the basic right of debtors to be treated honestly and with dignity throughout the process.

Federal Laws Protecting Debtors from Creditors

1. Fair Debt Collection Practices Act (FDCPA)

The Fair Debt Collection Practices Act, or the FDCPA, is among the significant federal statutes of America that is specifically penned to safeguard the rights of debtors. The key statute establishes stringent guidelines and norms regarding the activity of third-party collection agencies while attempting to collect debts that are due by individuals.

FDCPA prohibits debt collectors from:

- Threaten you with violence or jail.

- Call you after 9 p.m. or before 8 a.m. without permission.

- Persistently bothers you by making numerous phone calls without cessation.

- Misrepresent the amount of debt.

- They will phone you during office hours even though you have specifically told them not to.

2. Fair Credit Reporting Act (FCRA)

FCRA governs the reporting of debt to credit. Creditors may be challenged by holders of debt against:

- Contest incorrect data on credit reports.

- Request correction if debts are erroneously listed.

- Receive a free credit report yearly.

3. Bankruptcy Laws (U.S. Bankruptcy Code

The debtors may exercise the right of bankruptcy when they cannot settle their debts. Bankruptcy gives legal protection, terminates collection efforts, and can eliminate specific debts.

4. Truth in Lending Act (TILA)

This law ensures that lenders clearly convey the terms of the loan, interest, and fees without deceiving debtors.

- The Right to Receive a Written Notice of Accrued Debt

- Debt collectors must provide a written “validation notice” within 5 days of contact with you that informs you of how much money you owe and to whom.

The Right to Challenge the Debtor Facing Creditors

Right to Written Notice of Debt

Collectors must provide a written “validation notice” within 5 days of initial contact, explaining how much you owe and who the creditor is.

Right to Dispute the Debt

The debtors can challenge the debt by writing within 30 days of receiving the notice. The collector is supposed to provide evidence before continuing with the collection, should there be a challenge.

Right to Stop Communication

You can pen a cease-and-desist letter requesting that the collectors stop coming to visit you. They can only respond with legal notices thereafter.

The Right to Privacy

The debt collectors and creditors cannot advertise your debt to your employers, relatives, or even friends.

Right to be Free from Harassment

Debtors have the right to be free from abusive language, threats, or intimidation.

State Protections of the Debtor

Beyond the federal rules that apply nationwide, of note is the reality that individual states within the nation actually have their own unique debtor protection rules that apply. Such local rules might:

- Limit wage garnishment levels.

- Include exemptions for necessary property (house, automobile, retirement savings).

- Prolong existing statutes of limitations that run against efforts to collect debts.

These should be vetted by debtors, though, with the protections varying significantly by state.

Common Illegal Practices by Credit Card Issuers and Collectors

Even though rules have been set, rules are sometimes disregarded by some agencies and creditors. A few of the common rule breaches include:

- Harassment refers to the act of referring to the individual on multiple occasions during the day or using abusive language.

- False Claims: Claiming that someone will go to jail due to debts.

- Imposition of Unauthorized Charges: It is the act of imposing charges or amounts that were not agreed or stipulated specifically during the initial contract.

- Pretending to Be Law Enforcement: Presenting oneself to debtors by pretending to be law enforcement.

If you experience these ploys, you have the right to make formal complaints to the Consumer Financial Protection Bureau, or CFPB, by its common name, or you can contact the office of the attorney general of your state.

Legal Remedies Available to Debtors Facing Creditors

Negotiating with Creditors

Debtors naturally have the right to negotiate regarding settlements, to seek schedules of payments that can be adhered to, or to request that their interest rates applying to their accumulated debts be reduced. Notable to note here is that, a significant percentage of creditors prefer to receive partial debt owed to them rather than taking the chance of receiving absolutely nothing.

Officially Requesting to Verify a Debt

If you question that a debt is legitimate, you may ask that a debt be validated. The creditor will have to verify that the debt belongs to you and that the amount is accurate.

Filing for Bankruptcy

If debts cannot be handled, then bankruptcy may be the absolute final choice. Bankruptcy will immediately stop collection efforts, wage garnishments, and lawsuits.

Commencing a Legal Proceeding Against Creditors

If a creditor has violated the rights of a debtor, then the debtor can sue the creditor to recover damages, attorney fees, or emotional distress.

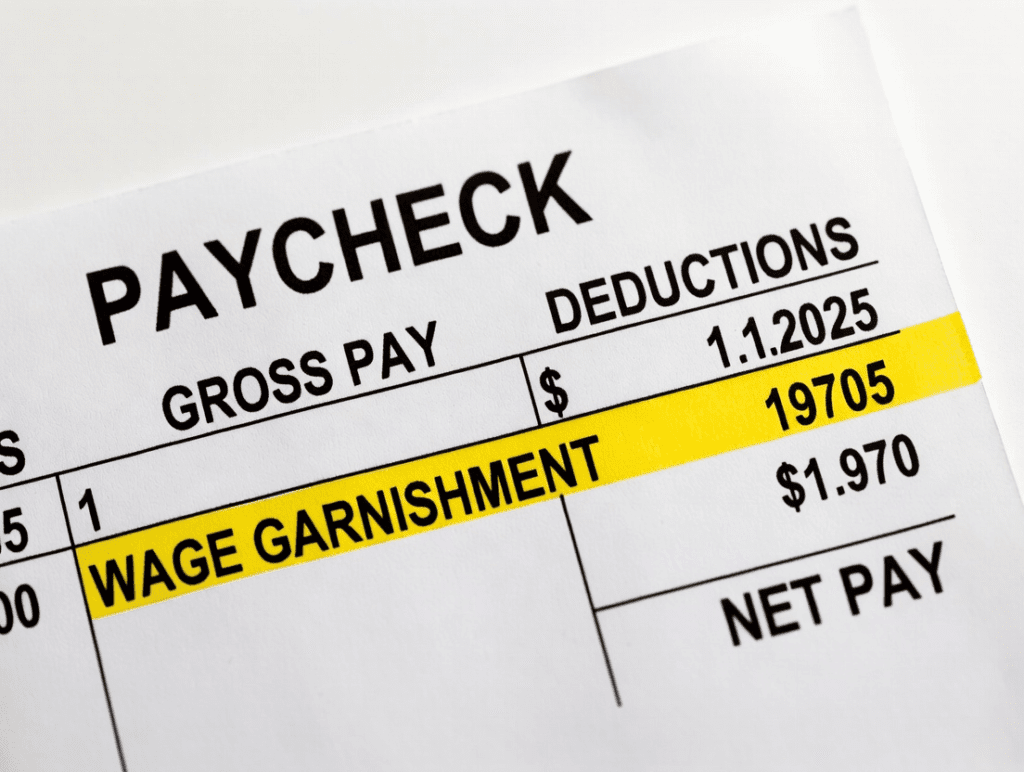

Rights of Debtor Under Wage Garnishment

Creditors can sometimes collect through wage garnishment (taking money out of your paycheck), but debtors’ rights abound:

- The federal statute only permits garnishment of up to 25% of the disposable income.

- Usually, Social Security benefits, including those pertaining to retirement and disability, are not typically subject to taxation.

- The debtors can challenge garnishment in a court of law if they experience financial difficulty.

Rights of Debtors in Situations of Confiscation of Property and Liens

- In the vast majority of cases, the creditors will typically require that they have a judicial judgment by a court system to legally place a lien against your assets.

- Certain of the assets, such as equity that accumulates on a primary residence or funds that are kept within retirement accounts, can be exempted by a citizen’s individual state codes.

- Creditors should be duly informed before the seizure of property.

How Debtors can Protect Themselves against Unlawful Practices

- Keep Detailed Records: Copies of all letters should be retained, every single email, and accurate call records.

- Communicate in Writing: Written communication creates proof in case of disputes.

- Understand Your Statute of Limitations: It is crucial to understand that debts that have been matured for a specified number of years can not be collected and hence cannot be litigated.

- Get Professional Legal Advice: Consumer litigation lawyers can defend you.

- File Complaints: Report violations to the CFPB, FTC, or State Regulators.

Rights of Debtors during Bankruptcy Actions

When an individual files for bankruptcy, debtors gain even more protection:

- Automatic Stay: Stops all collection activity effective immediately.

- Release of Debt: This procedure essentially discharges limited forms of unsecured debts, which the majority of times consist of balances that exist on credit cards.

- Preservation of Property: Bankruptcy exemptions can aid you in exempting your home, car, or retirement account.

Conclusion: The Role of Debtor Rights and Their Relevance

Debtors who owe money and have debt collectors after them might feel vulnerable, but they are safeguarded by the law. There are laws against harassing and against unjust wage garnishments. The debtor’s rights ensure that debt collection is reasonable.

By learning and practicing these rights, debtors can safeguard themselves, get preferable payment terms, and make enlightened decisions about payment of debts or bankruptcy.

Knowledge is the best safeguard that each of us can possess. By gaining a general overview of your safeguards with the law as a debtor, you will be better able to get your financial life together while, at the same time, insulating yourself against predatory creditors who will seize upon your situation.

(FAQs)

[…] debt settlement while being collected on by creditors, covering the process, negotiating tactics, legal rights and responsibilities, pros and cons, taxation, and advice on handling finances after […]

[…] An audit or legal consequences. […]

[…] Need more information about Legal Rights of Debtors: […]