Introduction: Why Negative Marks Are Critical

When you accept payment for a debt, it can be extremely helpful because it lets you literally close an account down and prevent larger issues from potentially happening, such as lawsuits or the risk of declaring bankruptcy. But there’s something important about paying a debt: it doesn’t necessarily erase the debt; it just places negative notations on the credit report that could have long-term effects. Those negative notations could significantly impact the credit rating and could remain on the credit report for some time, hampering the person’s financial future for as long as it lasts.

Knowing how long the adverse notations stay on your credit report after the settlement is very important if you want to properly project the time for the recovery of your finances, apply for applications for future loans, or restore your credit score over time.

What Are Negative Marks on a Credit Report?

It refers to undesirable entries placed on the credit report that may affect the creditworthiness negatively. Its types include the following:

- Missed or late payments

- Charge-offs

- Settlement

- Defaults

- collections

- Bankruptcies

All of these signs constitute an open warning for lenders that you encountered challenges paying off the debts properly. The act of settlement falls directly into this category, as it implies that you could not pay the full share that you initially owed.

Why Does Settlement Result in Negative Marks?

A settlement is an official arrangement between you and your lender where you pay an adjusted sum, less than the original balance. Though the deal helps you avoid total default on the payment of your finances, it still implies the lender incurred a financial loss due thereto. Credit agencies mark the account as ‘Settled.’ Lenders view this status as less desirable than a ‘Paid in Full’ classification.

How long do adverse marks stay on credit reports after settling?

The precise time for staying may significantly depend on the actual type of the specific type of entry:

- Settled Accounts: Are valid for 7 years, counting from the settlement date.

- Late Payments Ending up in Settlement: Stay for 7 years after the missed payment date.

- Charge-Offs Before Settlement: Stay for 7 years after the charge-off.

- Collection Accounts Related to Settlement: Also continue for 7 years from the initial delinquent date.

Important: It’s crucial to understand that while these NEGATIVE notations might appear on your credit report for some years, their effect and significance decrease further as time progresses. The older an entry is on your report, the less effect it contributes to the calculation of the total credit score.

Impact of Negative Marks on Credit Score for Settlement

The way minus points work for you follows below:

- Score Decrease Due to Settlement: It decreases the score by 50 to 100+ points.

- Payment Default: You might not meet the payment deadlines.

- Credit Score Downgrade: Banks may lower.

- Higher Rates of Interest: In the event the application gets accepted, you could end up paying higher interest.

- Lower Credit Limits: Credit card issuers may limit how much you borrow.

While the harm is actual, it’s not irreversible; you will be able to restore credit even as there are marks.

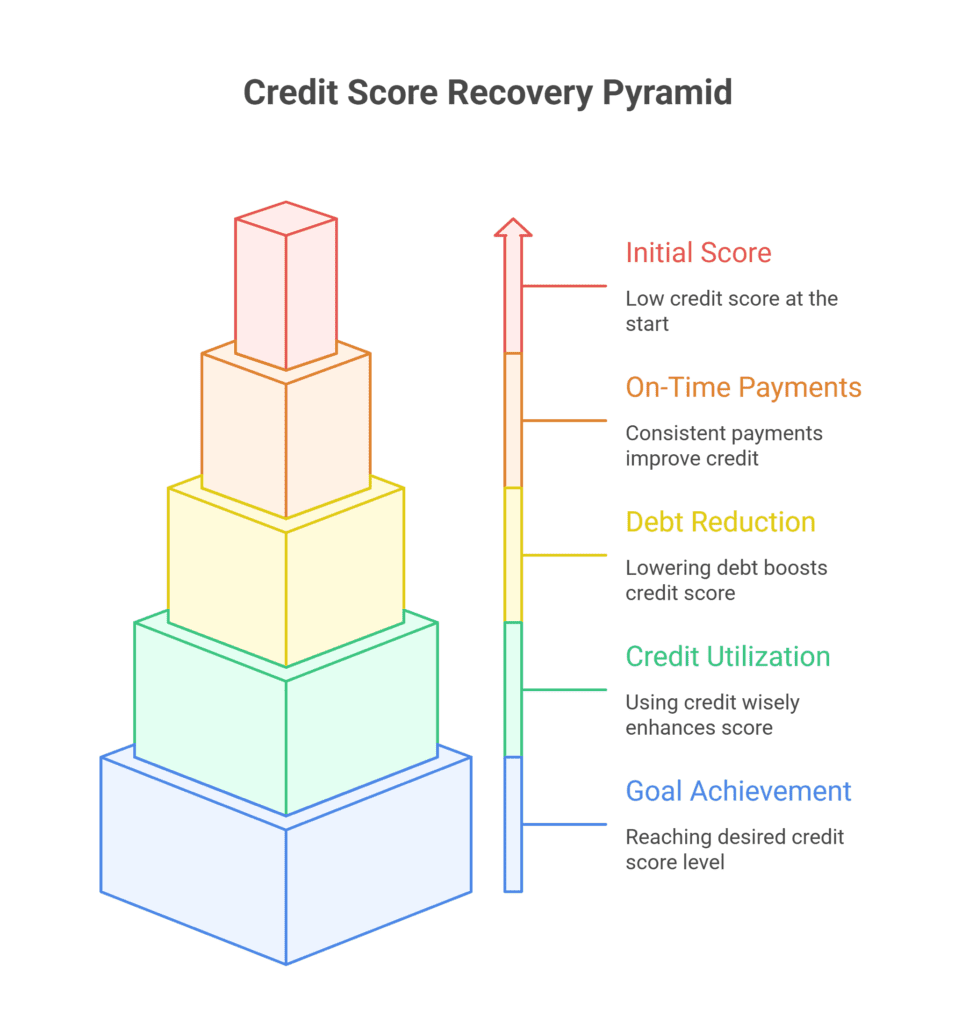

Advantages of Policy on Resolution Timing

Year 1 Significant Impact

- Your score experiences the most significant decline, resulting in the hardest hit.

- The lenders see you as being at risk.

- It’s difficult to obtain new credit.

2 to 3 Years’ Effects Start Winding Down

- The adverse notation stays on your credit report; however, when you continue making on-time payments for the rest of your accounts, you will notice an improvement in your credit score.

- Certain banks might allow for small amounts, but at larger interest rates.

Years 4 to 5 Moderate Impact

- The lenders also pay less attention to old settlement entries.

- A positive payment record then becomes increasingly important and effective compared to the existing adverse record.

Years 6 to 7 Impact That Is Minimal and Insignificant

- The sign still technically exists, but it has little effect or impact.

- After a duration of 7 years, the entry regarding the settlement will automatically be removed from your credit report.

Techniques for Reducing the Adverse Effects of Negative Marks

You don’t abolish valid settlements in 7 years, but you may reduce the impact:

- Be Sure That All Future Bills Are on Time and on schedule. Keeping up on payments on time is important in helping to correct and equalize past fiscal errors.

- Maintain Low Credit Utilization. It’s advisable not to use credit beyond 30% of the available credit you hold.

- A combination of Credit Types, carrying credit cards + loans with regular payments, enhances credibility.

- Limits the Number of Annual Credit Applications. Applying for credit too many times in the span of one year could decrease the credit rating.

- Use Secured Credit Cards. These credit instruments assist in quickly restoring a credit score but provide for secure and controllable limits, not allowing for excess spending.

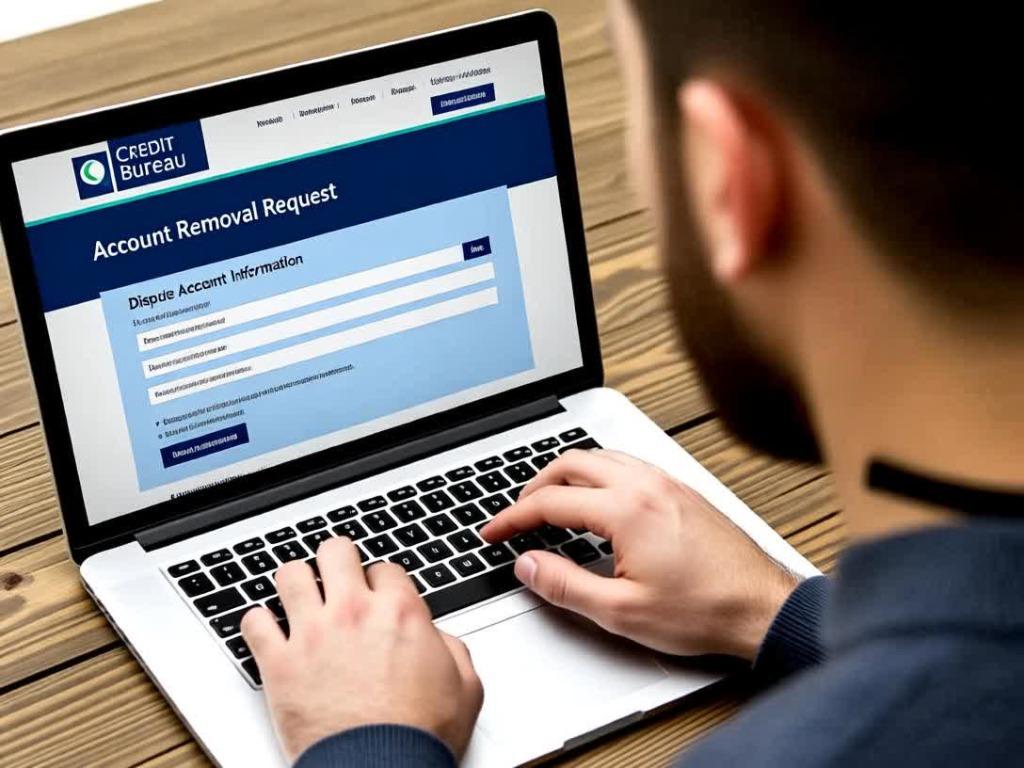

Can You Remove Negative Marks after an Early Settlement?

Indeed, in some circumstances and some instances:

- If the bureau failed to update the balance or entered it twice, you can challenge and correct the error.

- In discussions toward making a “Pay for Delete” deal, while this situation, as described, is not all that common, some lenders or collection agencies can agree to strike the adverse comment on your credit report. Lenders generally remove the mark if you settle the outstanding debt and submit a legal deletion request in writing.

- Engage the Service of Credit Repair Agencies: What they do best includes disputing as well as negotiating for early deletion.

Warning: In the event the mark proves valid and accurate, it will not, in general, be erased by credit bureaus until the time.

Legal Rights as Provided under the Fair Credit Reporting Act (FCRA)

The FCRA protects consumers against unfair reporting. Within this statute:

- Collection agencies will not maintain the adverse notations for more than 7 years, except for bankruptcies for 10 years.

- You can appeal mistakes at any time.

- In the case that data is proven to be false or inaccurate, bureaus shall either correct or remove the data within 30 days at the latest.

- In the event you realize that the bureau or the lender will not correct false data reported, then you technically have the right to sue them for Damages.

Settlement Compared to Other Negative Marks: Comparing the Length of Time

| Negative Mark | Duration on Report | Severity |

| Late Payments | 7 years | Moderate |

| Settled Accounts | 7 years | Moderate to Severe |

| Charge-Offs | 7 years | Severe |

| collections | 7 years | Severe |

| Bankruptcy (Chapter 7) | 10 years | Very Severe |

| Bankruptcy (Chapter 13) | 7 years | Severe |

This comparison shows that settlement is damaging but still less severe than bankruptcy.

Reestablishing Credit Record While Negative Marks Remain

Even when you won’t erase marks at an early stage, it’s possible to restore the profile:

- It’s important to set up an informed budget and stick to it diligently. Planning ahead will prevent you from missing payments later on.

- Make the most of Automatic Payments. Never miss payments by mistake.

- Apply for a Secured Credit Card to build credit in the right way.

- Requesting higher credit lines also comes in handy, as it ends up decreasing the utilization ratio.

- Regularly Checking Credit Reports. This allows individuals to identify and spot any errors at an early stage.

- Become an Authorized User on someone else’s good credit account.

Over time, these positive actions will overshadow old marks.

Conclusion:

Settling a debt is a crucial step toward closing an account. However, you must remember that this action places negative marks on your credit report for up to seven years.

While these marks damage your credit score most in the first few years, their impact fades over time. Instead of waiting, you can improve your financial standing through consistent, positive credit habits. By doing so, you can rebuild your score long before the negative notation disappears.

To succeed, you must understand your rights, dispute any errors, and maintain a solid repayment record. Though perhaps not the very best possible outcome, it’s at least significantly more desirable than choosing not to do something about the state of being in debt at all or later suffering the dire consequences of bankruptcy.