Introduction: When Debt Forgiveness Becomes a Tax Bombshell

If a debt is paid, a portion of it is forgiven, or a lender releases it, it’s a kind of relief, but some weeks afterwards, a piece of mail arrives, Form 1099-C (Cancellation of Debt). Many a borrower frets, but it’s seldom worse news than it appears.

Form 1099-C is how the IRS is notified of a part of your debt being forgiven/canceled. What not many people are aware of, however, is that the IRS typically regards as taxable income debt that’s been canceled, which your taxes then might end up being increased for if not avoided appropriately.

Learn here about Form 1099-C, what it is, why it’s being sent, when it’s possible to not pay taxes on it, and how to report it yourself to stay clear of IRS trouble.

1. What is Form 1099-C Actually?

Form 1099-C is a statement written by a lender or creditor if a debt of or over $600 is written off, cancelled, or forgiven. It notifies both you and the IRS of a debt previously owed by you that no longer exists.

It’s written most frequently when:

- You pay a loan for fewer pounds than are owed

- A lender writes off your outstanding balance

- That a credit card, health, or personal loan is written off

- Foreclosure, also known as repossession, takes

- Student loans are discharged for certain programs

By statute, your creditor is required to send a copy of this form by mail by January 31st of the succeeding year, and also furnish a copy to the IRS.

In simple terms:

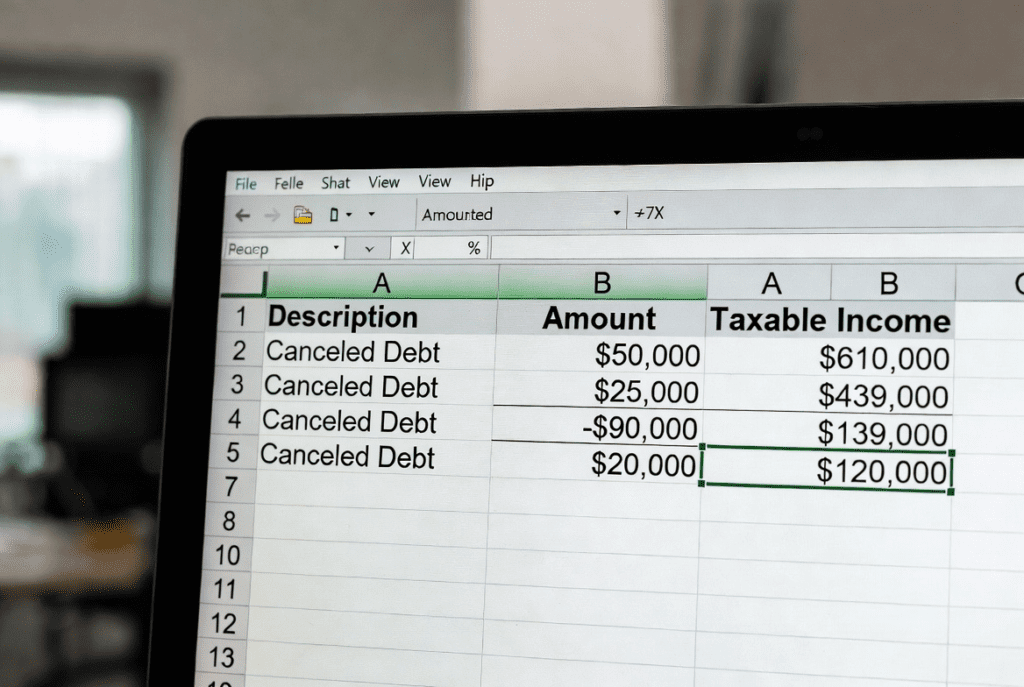

- If you owed $10,000 and paid off $6,000, then the $4,000 that was forgiven might be listed as “income” on Form 1099-C.

2. Why Does IRS Treat Debt That’s Cancelled as Income?

The IRS views debt cancellation as income since, technically, you did receive a benefit of that money when you owed a debt. If a lender forgives your debt, it’s as if you “earned” money that came, and it did not have to be paid back.

That is why it may be included in your gross income on your tax statement.

For example:

- You borrowed a personal loan amount of $8,000.

- You settled it for $4,000.

- The lender pays off the remaining $4,000 and sends a 1099-C.

- Those $4,000 can be included in your taxable income.

But there are some major exceptions, which prevent you from having to pay taxes and here’s the thing, not everybody knows about it.

3. When You Might Not Pay Taxes on Debt That’s Forgiven

Not all of your debt forgiven is taxable. Here are examples of times when your write-off amount may be exempted from your income:

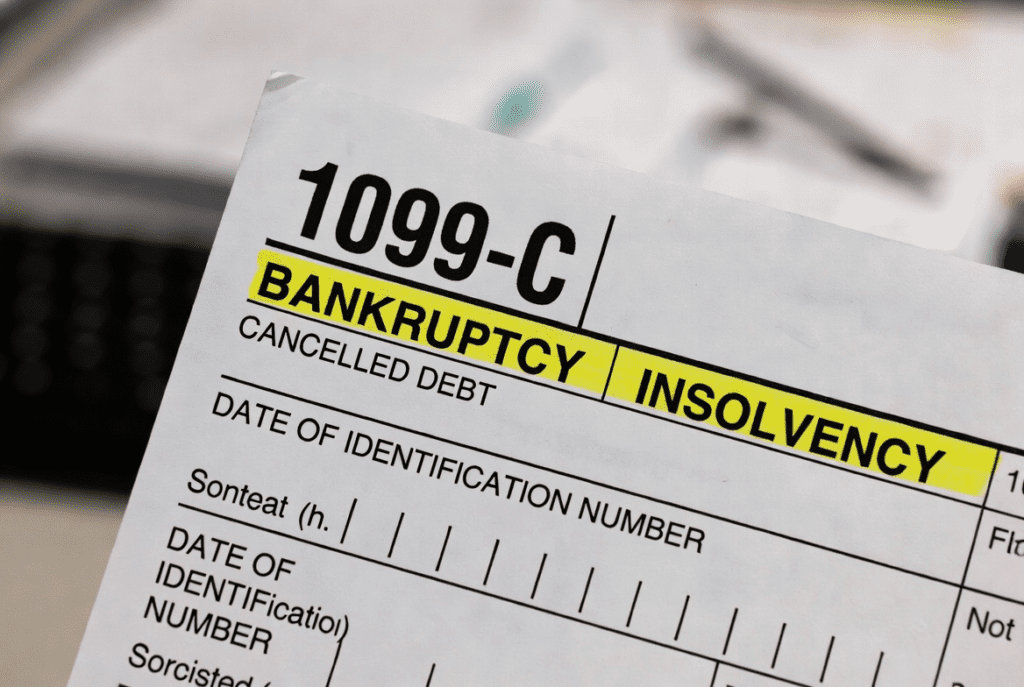

a. Insolvency

If it did happen that you were insolvent, i.e., your liabilities exceeded your total assets at the time your debt was eliminated, then, of course, you wouldn’t owe taxes on debt eliminated.

You are required to file IRS Form 982 to be eligible for this exclusion and to select your situation as of the date.

b. bankruptcy

If bankruptcy releases your debt, it’s not taxable. Debt releases by bankruptcies are exempted by legislation from income.

c. Some Student Loan Forgiveness

Federal loan forgiveness under the Public Service Loan Forgiveness (PSLF) or the Teacher Loan Forgiveness is exempt from taxation on the federal level.

Read more about Public Service Student loan:

d. Mortgage Forgiveness Relief

Some of your mortgage debt relieved by way of foreclosure, short sale, or modification is potentially excludable by virtue of the Mortgage Forgiveness Debt Relief Act (extended some years).

e. Business Loans

If it’s a debt for your business or self-employment, qualified tax rules are involved. You are permitted to deduct part of your loss.

By discovering which exemption can be yours, you can save yourself hundreds or thousands in tax.

4. What Does Report Form 1099-C?

This is what all the paragraphs on the form are about:

| Box | Description | |

| 1 | Date of identifiable event (when debt was canceled) | |

| 2 | Amt of debt waived | |

| 3 | Interest (if included) | |

| 4 | Duration of debt description (loan type, account) | |

| 5 | If the borrower became personally liable, 6 Reason for cancellation (settlement, bankruptcy, etc.) | |

| Creditor Information | Cryptor’s name, street address, and taxpayer identification number | |

| Debtor Information | Your name, street address, city, and state | |

Check absolutely everything, including money and data, before you enter your taxes. It is very easy to make errors.

5. What to Do with Form 1099-C on Your Tax Form

If You Receive Form 1099-C:

- Verify for accuracy: confirm the lender information and amount are correct.

- Decide whether it’s taxable: check IRS requirements or speak with a tax agent to find out if it’s exempt.

- If it’s taxable, report it as “other income” on your tax return.

- If it’s excluded (e.g., due to insolvency or bankruptcy), file Form 982 to explain why.

- Keep records: the IRS can ask for documentation 7 years after the event.

You should usually hire a qualified tax preparer if your case is complicated or if it includes numerous debt cancellations.

6. Example: The Operation of a 1099-C in Real Life

David, just one example, carried a combined credit-card balance of $15,000. He had paid off a $9,000 bill after being laid off.

The credit card firm waived off the remaining $6,000 and issued a 1099-C to him come January.

Here’s how it works:

- You inform the IRS of $6,000 of debt forgiveness.

- David must figure out if he is taxable for $6,000.

- If his total liabilities surpassed his assets, then he himself could plead insolvency and forgo tax on the amount written off.

- Otherwise, that $6,000 is considered taxable income for him during the year.

7. Common Situations Which Warrant a 1099-C

You may receive it after events such as:

- Settlement of debt

- Foreclosures or short sales

- Credit card write-offs

- Repossession of a car or property

- Cancellations of personal loans

- Student loan relief

- Abandoned property or relinquished rent liability

Even if you did not actually pay your debt, lenders are able to give a 1099-C if they write it off their ledger.

8. How to Challenge Mistakes on Form 1099-C

Errors are normal. If you think the form is incorrect:

- Call the creditor at once and ask for a proper form.

- Retain all settlement letters or payment receipts as a record.

- If your lender fails to fix it, you may submit a written statement explaining it to your tax return.

- Finish your return as accurately as possible and give the IRS a chance to review your paperwork.

Do not leave off the format; even if it’s incorrect, it’s submitted to the IRS anyway, and not having it might cause a notice or an audit.

9. Debt Settlement Companies and Processing of 1099-C

If a debt settlement company assisted you, they might not tell you that the eliminated debt may become taxable income.

As an example, if you settle several credit card accounts, you may end up getting a distinct 1099-C for each one of them. That’s why it’s really important to plan ahead and perhaps negate that income through deductions/exclusions.

Inevitably, preserve all settlement agreements; they’ll come in handy if, at some point, you need to establish the reason for cancelling.

10. The Emotional Side: Don’t Panic When You Get It

Most people are scared or confused if they receive a 1099-C, thinking they must have done something incorrectly. It’s actually just a statement sent by the IRS to notify it of a debt being forgiven for you.

Treat it like a tax form, not like a notice of collection. You are not actually being reassessed by your creditor; you are merely being asked to report it appropriately for tax purposes.

11. Procedures for Avoiding Future Tax Liability for Forgiven Debt

You pay ahead to try to keep your chances of large tax bills low:

- Manage your finances, keep a statement of your assets and liabilities (proves your bankruptcy).

- Get a tax advisor before settling on a settlement.

- Ask about their reporting-in policies before reaching any agreement with them.

- Pay your tax in advance and don’t wait until the very end.

- If possible, negotiate decreased amounts or pay periods instead of complete dismissal.

Accurate planning helps you avoid unexpected taxes when it’s your turn next.

12 Common Mistakes About 1099-C You Should Avoid

Myth #1: “I don’t have to tell if I didn’t receive the form.”

→ False. Even if it’s eliminated, it’s possible the IRS might be informed through lender reporting.

Myth 2: “Settled debt is never taxable.”

→ False. It might be taxable unless it’s exempt for you.

Myth #3: “The lender cannot issue 1099-C after bankruptcy.”

→ False. They are qualified to provide it, but it’s nontaxable; you just report it on Form 982 to reflect that.

Myth #4: “I can ignore it because it’s small.”

→ False. Even small quantities are sufficient to notify the IRS.

Conclusion:

Be Smart, Not Scared, about 1099-C Form 1099-C may seem intimidating, but it’s actually just a record, not a penalty. It notifies the IRS of a portion of your debt being written off. Even though it, at times, generates taxable income, many are exempt, and it’s eliminated or reduced in tax effect.

The thing to do is organise yourself, know your rights, and have a qualified tax preparer assist you. Whether your debt was settled, discharged by hardship, or relieved by some relief program, doing the tax end of it right helps your new life financially stay stress-proof.

[…] Read more about debt cancellation tax rules: […]