Introduction

Once you actually settle a debt, it’s a tremendous weight off your shoulders. You’ve haggled with your creditors, paid off bills in a large sum, and decreased your debt burden, a huge financial success.

But by starting to recuperate, a crucial question occurs:

“Wilt thou be accepted for other loans, e.g., a mortgage, after settling thy loans?”

The reality is, your credit profile is impacted by debt settlement, and it does have some impact on lenders evaluating you in the future. It definitely doesn’t mean, however, that it would be impossible to approve new credit lines. If you’re prudent, waiting, and reorganizing your finances, there’s no doubt you can rebuild lender trust.

This piece examines the real impact of debt settlement on your potential loans and mortgage eligibility, lenders’ demands, how to recover your creditworthiness, and how soon it recovers.

1. Comprehending how Debt Settlement impacts Your Credit Report

As you settle a debt, your creditor notates your credit report to say that the account is “Settled” or “Paid – Settled for less than the amount owed.”

Here’s what that means:

- Settled: You paid fewer dollars compared to how much money you owed.

- Paid in full: You paid the full sum.

- Charge-off: Your creditor charged off your overdue debt before settlement.

These creditors, when they view your report, will see this notation and recognize that you paid off less than your original obligation, which can raise suspicion about repayment reliability.

But whereas bankruptcy reveals a failure to pay your debt, settlement reveals that you did your due diligence to pay it off, a better barometer for the long term.

2. What Debt Settlement Does to Your Credit Report

Settling debt generally leads to a brief, temporary credit score decrease. The extent of decrease is based on several factors:

- Number of settled accounts

- Number of debts released

- Your credit history before settlement

- Payment record (late or missed payments)

impact example:

- If your credit score was 720 before settlement, it may finish at 580–620.

- If your own score was similarly low (less than 600), then less harm is caused, as your report also showed a high risk anyway.

The silver lining is that credit scores recover eventually, ideally if positive behavior continues after settlement.

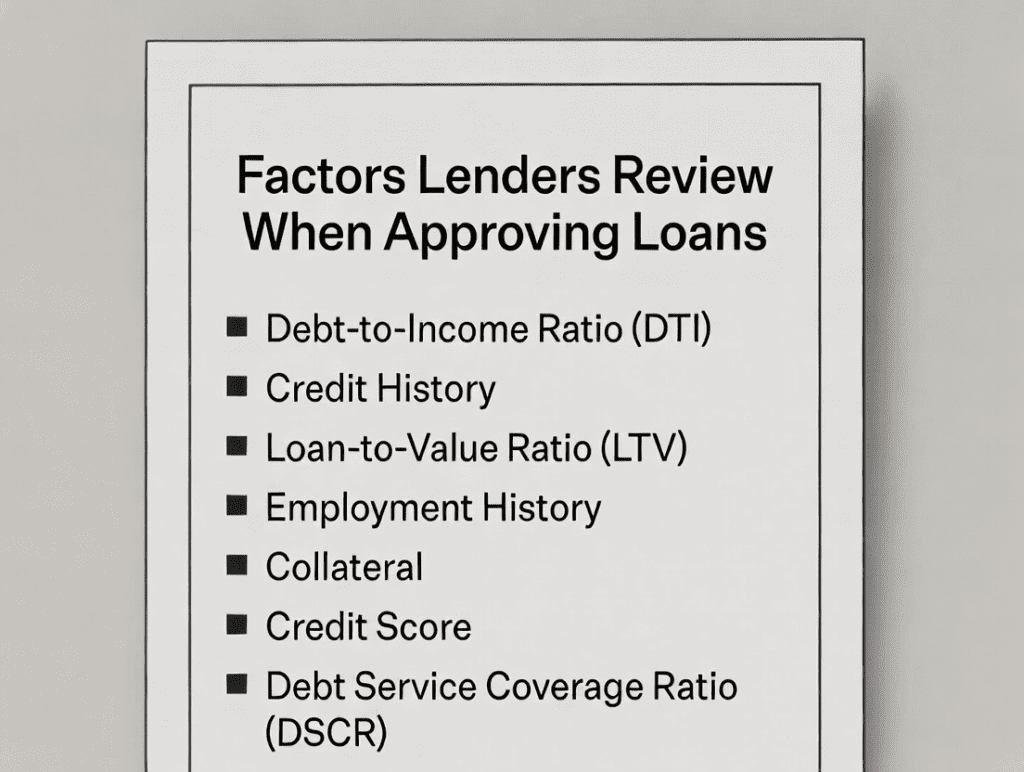

3. The Lender’s Perspective: How They Treat Paid-up Debts

Lenders, banks, and mortgage companies assess your financial behavior, not just your score. Here’s what they consider:

| Lender Concern | What It Means | Your Response |

| Settlement history | Indicates past financial stress | Show improved stability and savings |

| Credit score | It shows current reliability | REBUILD CREDIT RESPONSIB |

| Time of settlement | More time = less risk | Issues related to the ability for payments |

| Current debt-to-income (DTI) ratio | Issues related to ability for payments | Reduce your DTI before application |

| Recent payment behavior | Shows whether you learned from past mistakes | Keep accounts current and error-free |

In brief: The longer ago it is and the better your recent form, the less settlement it counts for.

4. Impact on Personal Loan Upon Settlement

Short-Term (0–12 months):

It is difficult to achieve a personal loan soon after settlement. Your recent settlement is viewed by lenders as a red flag, a sign of potential financial instability. You are only qualified for:

- High-interest loans, or

- Secured loans (against collateral).

Medium-Term (1–3 years):

As your payments are up to date and your score recovers, lenders are more inclined to give you money. It’s possible to raise your chances by:

- Having a stable income,

- Having low credit utilization,

- Show evidence of savings or security.

Long-Term (3+ years):

3–4 years later, lenders recognize your paid-up accounts as “aged” records, especially if your credit report shows a smooth trend of improvement.

5. Car Loan Impact After Debt Resolution

Car finance is easier to obtain once settled than a mortgage or secured personal loan, but interest premiums may occur at inception.

Tips to boost chances of approval:

- Apart from a larger down payment (20% or larger).

- Apply through local credit unions – they are normally less stringent on loan parameters.

- If available, a co-signer (good credit) should be utilized.

- Show evidence of stable income and employment.

With time, timely payments on a short auto loan actually work to rebuild your credit more rapidly.

6. Can You Purchase a Home after Settlement?

Yes, it’s certainly possible to buy a home after debt settlement, but it’s a case of preparation and timing.

They are wary because a settlement means you have a pre-existing issue of debt. They are, however, more concerned about your recovery time, rather than your previous error itself.

7. Debt Settlement and Loan Approval

The mortgage underwriters review three key sectors:

- Credit History: Settled accounts signal past hardship.

- Income & Stability: Lenders need assurance that you can handle new payments.

- Down Payment & Reserves: A bigger down payment decreases perceived risk.

You might have to wait for periods before being qualified for a mortgage, depending on your lender and loan.

8. Average Wait Period Before Mortgage Approval

| Type of Loan | Waiting Period After Settlement | Requirements |

| Conventional Loan (Fannie Mae/Freddie Mac) | 2 years recommended | Strong credit recovery & 20% down payment |

| FHA Loan | 12–24 months | characterize stable employment, clean pay |

| VA Loan (Veterans) | 12 months | evidence of re-established credit |

| USDA Loan | 3 years | Must be a good money manager |

The longer it takes and the better your credit profile, the larger your chances of obtaining approval and better interest rates.

9. Re-establishing Credit to Qualify for Subsequent Loans

Having settled, your fastest way to recover your credit standing is through steady and wise rebuilding.

Main Strategies:

- Pay all current bills on time.

- Pay less than 30% of your credit utilization.

- Apply for secured credit cards or credit-builder loans.

- Do not apply for a number of accounts simultaneously.

- Ensure stable employment and income verification.

With effort, numerous individuals witness their scores increase by 100–150 points in 18–24 months.

10. Improving Debt-to-Income (DTI) Ratio

Your DTI ratio is one of the most significant determinants.

It measures how much of your monthly income goes toward debt payments.

Optimal DTI for Loans:

- Under 36% for traditional loans

- Below 43% for government-insured loans, FHA, etc.

Once settled, your DTI also improves by default since your debts decrease, but if your borrowing becomes excessive before a reasonable settlement figure, your DTI may surge upward again. Therefore, keep a balance between borrowing and savings.

11. Secured vs. Unsecured Credit After Settlement

They can initially provide secured credit products, such as:

- Secured credit cards

- Credit-builder loans

- Collateral-secured personal loans

Once you have been demonstrating steady payments, your unsecured credit lines are yours again.

These slow reconstruction efforts display the budget responsibility that lenders prefer.

12. How lenders view “settled” vs “charged off” accounts

| Status | What It Means | Lender’s View |

| Settled | You negotiated and paid part of the debt | Moderate risk shows effort |

| Charged-off | Debt was written off without payment | High risk shows nonpayment |

| Paid in full | Full repayment | Low risk ideal |

That is, a settlement is good compared to a charge-off but inferior to a pay-in-full.

But it’s a huge step towards reclaiming your credit reputation.

13. How Long Settlement Affect Your Credit Report

Payments settled remain for 7 years on your credit report, starting from the date of delinquency.

But it becomes ineffective after some time.

- Years 1–2: Severe adverse effect

- Years 3–5: Moderate effect

- After Year 5: Little to no effect if your current record is clean

Therefore, if you are planning for a mortgage, it’s a good idea to wait at least 2–3 years after settlement before applying.

14. A Co-Borrower or Co-Signer Using

If your credit did not recover, it may work to your benefit to go in with a reputable co-signer (family, spouse, or significant other) who has great credit.

Their good credit history offsets your risk profile.

Just ensure:

- They truly know their responsibility (they are legally accountable).

- You make all payments on time to protect their credit.

15. Getting Pre-Qualified vs. Pre-Approved After Settlement

- Pre-qualification is a soft inquiry that estimates your eligibility.

- Pre-approval depends on a clean check of your finances, including your settlement record.

Begin with pre-qualification to test your position without affecting your credit record, and work your way towards pre-approval when your credit record is better and your finances are stronger.

16. The Down Payment and Savings Role

A larger deposit (15-25%) greatly enhances your mortgage application after settlement.

It shows the strength of funds and limits exposure for the lender.

Also, having liquid funds for 3–6 months of mortgage repayments greatly enhances your approval chances.

17. How to Notify Debtors of Debt Resolution

It’s a good thing to be transparent when getting a mortgage loan. Give a brief-written statement saying:

- Why did you settle your debts (medical issues, job loss, etc)

- Whatever you’ve done to recover financially

- Proof of improved payment behavior

This shows responsibility and maturity traits lenders like to see.

18. Avoiding Common Errors After Settlement

- Applying for Credit Too Quickly

- New account charges for late payments

- Neglecting your credit report

- Not being prepared for emergencies

- Closing older accounts (decreases credit age)

Avoiding these mistakes accelerates your recovery and improves loan approval chances.

19. Loan Qualification Chronology After Debt Resolution

| Time After Settlement | What to Expect |

| 0–6 months | Rejection likely; focus on rebuilding |

| 6–12 months | Might be qualified for secured or high-interest loans |

| 12–24 months | Better marks; approval for auto and personal loan |

| 24–36 months | Qualified for FHA/VA loans w/ good standing |

| 36+ months | Solid credit recovery; traditional loans are possible |

You should be regular and persevering.

20. Speed Up Your Mortgage Readiness Steps

- Pay all bills due now before the due date.

- Maintain reserves of 3–6 months.

- Lower average credit utilization.

- Correct any incorrectly credited postings.

- Keep older accounts open to preserve credit histories intact.

- Speak to a credit counsellor if necessary.

In a space of 24 months, your profile can change “risky” into “reliable.”

Conclusion

Debt settlement becomes a temporary blight on your credit record and a turn-off for new loan or mortgage facilities, but it’s far from a death blow for your ability to borrow. Rebuild your creditworthiness by being responsible, disciplined, and patient regarding money management.

Stress frequent, on-time payments, savings, low DTI, and lender disclosure. You are eligible for personal loans, auto loans, and even home mortgages in a few years, usually at competitive interest rates.

Debt settlement provides you a second chance: don’t waste it to create a future of money independence and security.

FAQs

[…] Their future loan approvals might be harder. […]

[…] In this piece, we are going to discuss what residuals are after a debt settlement, how to handle them responsibly, and how to recover a sense of value and money management for the future. […]