Introduction

When multiple parties, such as cosigners or co-borrowers, share a credit account, the loan intertwines their finances indefinitely. This arrangement becomes complicated when an individual attempts to settle a debt for less than the original balance.

Debt settlement is a helpful way of reducing what you owe, but it also creates ripple effects that potentially hurt or ensnare other parties listed on the account. Cosigners and parties who are joint holders of an account may endure credit harm, threat of collections, or legal liability even if they themselves never missed a bill.

In our article, we’ll examine exactly how settlement affects cosigners and joint account holders, what statutory rights each person has, and what smart steps both sides should take for protection.

1. Understanding about Cosigners and Joint Account Holders

As preparation for settling influences, it’s also useful to understand how both are different:

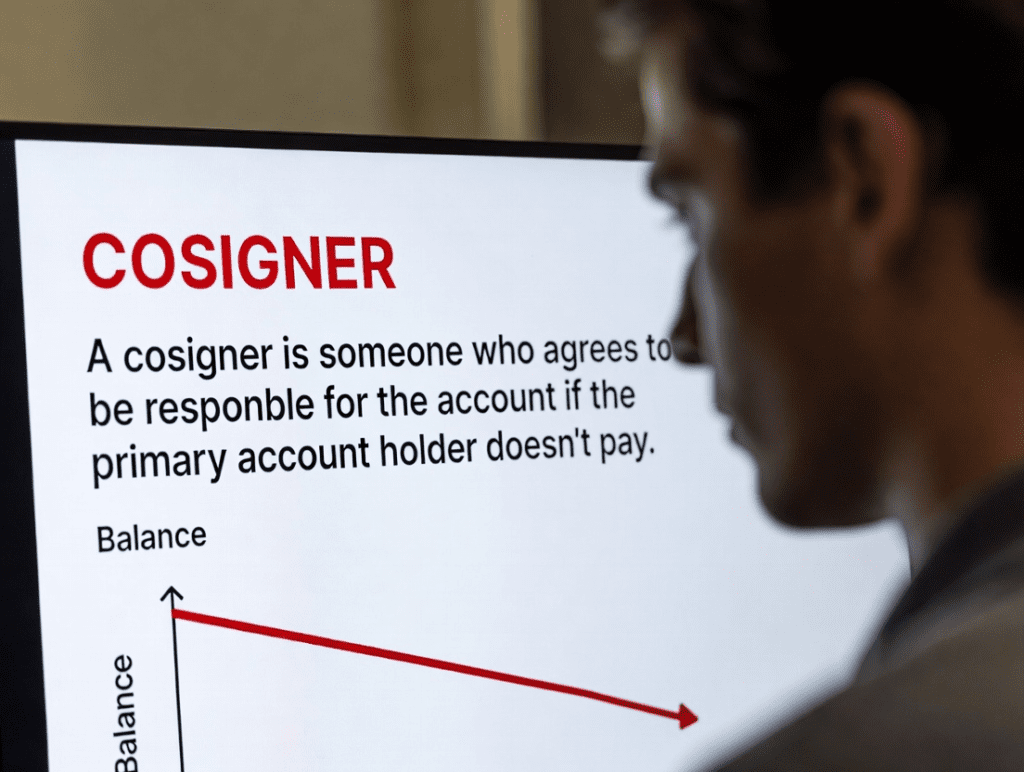

Cosigner

The cosigner also promises to pay for the debt if the main borrower cannot pay it back.

e.g., Your parent cosigns your car loan, so you are qualified for better loan conditions.

Co-Borrower (Joint Account Holder)

- As a joint account holder, a person becomes equally responsible for the debt from its origin.

- Case Study: You and your husband/wife both simultaneously apply for a loan or credit card.

Major distinction:

- A cosigner does not benefit from the money but guarantees to pay if necessary.

- Any co-borrower utilises the account actively and becomes equally responsible for the debt.

In both scenarios, the law legally allows creditors to pursue both parties for a full settlement.

2. What if You Pay Off a Joint or Cosigned Loan?

Once you pay a debt, the creditor accepts a smaller amount as ‘payment in full’.

But it impacts both sides interested in that debt:

- The settlement will revise the credit reports of both parties.

- The creditor might file any remaining forgiven amount with the IRS as taxable income.

- Creditors may hold the co-signor/co-borrower responsible if they do not appropriately ratify or complete the settlement.

Therefore, even when a settlement grants a release to the principal debtor, it can bring about unintended consequences to other parties.

3. Credit Scores’ Effect on Cosigners and Joint Debtors

For Cosigners

If the borrower pays less than they owe, the creditor lists the account as ‘settled for less than full balance.’

This adverse comment is on both credit reports.

Hygiene:

- Cosigner’s credit score may decrease by 50-100 points.

- Their future loan approvals might be harder.

- The account remains visible for 7 years from the settlement date.

For Joint Borrowers:

Both spouses’ credit reports reflect the same updates, so if one person pays, the creditor reports both as paid.

Even if a single individual wished to keep on settling, the report shall reflect the whole account settled, not paid in full.

4. Legal Liability Following Settlement

Whose Responsibility Remains?

If it’s duly recorded, both parties are released by the creditor for any additional liability.

However, if settlement letters are for a single borrower, then a subsequent borrower is still legally liable for whatever sum remains.

e.g.:

- You and your friend have a shared credit card with a $6,000 bill.

- You pay your share of $3,000.

- If the contract does not release your friend, then the creditor can recover the additional $3,000.

That is why settlement letters must specify all parties at fault.

5. When Only One Party Negotiates a Settlement

At times, even the primary borrower tries to pay off without notifying the cosigner or joint borrower. That engenders law and credit issues like:

- The cosigner’s credit is being damaged unexpectedly.

- Collection agencies are contacting the cosigner for the remaining sum owed.

- Conflict of relationships due to unforeseen liability.

The creditor also does not need authorisation from the cosigner whether to settle for an arrangement, but both of them know it simultaneously if it occurs. That’s why you need to communicate before negotiating.

6. How Settlement Figures on Credit Reports

When you settle the account:

- The status is “Settled” Paid for less than the full amount.”

- This same notation appears on both borrowers’ credit reports.

- The settlement date becomes the start date for the record period of 7 years.

Even if both borrowers do not participate directly, the settlement mark still affects them both because credit agencies treat joint accounts as co-responsible.

7. Taxation Consequences for Cosigners & Joint Debtors

When you pay off a loan, the IRS generally taxes any unpaid (forgiven) portion exceeding $180.

For example:

The creditor reports the remaining $4,000 on Form 1099-C. (Cancellation of Debt Income).

Depending on how the creditor reports the debt:

- The creditor typically sends the form to the primary borrower.

- The IRS considers both parties liable for tax consequences on a joint account.

Always consult a tax professional to avoid double taxation or misreporting.

8. What If the Borrower Defaults After Settlement?

If a borrower promises to pay by instalments but fails to pay, then a creditor can:

- Void the settlement agreement.

- Re-credit the full amount.

- Collect money from the cosigner or co-borrower.

creditors can hold the cosigner responsible even if you paid off the debt.

You should receive settlement funds and have it documented in writing.

9. Obtaining Joint Borrowers and Cosigners During Negotiation

If you plan to settle a debt that involves another person, follow these steps:

- Let the other party know soon, don’t surprise it by settling.

- Get written consent of all parties before it’s finalised.

- Request the creditor to mention both names on the settlement release correspondence.

- Make sure both sides are noted as “settled in full.”

- Retain all written documents, letters, e-mails, and receipts.

This guarantees the creditor is unable to subsequently pursue the other borrower for pay-outs.

10. The Role of Debt Settlement Companies

If you work with a debt settlement firm, let them know if your debt carries a cosigner or co-borrower. Many firms don’t define it, which causes grave difficulties.

Without proper documentation:

- The settlement may release only the primary borrower.

- The cosigner might still face collection or lawsuits.

Naturally, also read the fine print and be certain the firm treats joint accounts responsibly and honestly.

11. If Someone Wants Out as a Cosigner

In fact, once a loan is signed, cosigners cannot withdraw.

They cannot, however:

- Ask for a cosigner release by your lender (some loans allow it after being paid regularly).

- Refinance the loan by the primary borrower’s name only.

- Ask for a signed liability waiver once the settlement is finalised.

They also shield the cosigner’s credit reputation when paid off through debt.

12. Paying Off a Debt Without Damaging Relations

Many of its cosigned or joint debts are between family members, partners, or friends. Decisions to settle can also strain those relationships. Avoid conflict by:

- Speak openly before settlement action.

- Explain your financial reasons clearly.

- Show proof of both sides’ credit and legal protection.

- If required, bring a financially savvy adult to serve as an impartial mediator.

Transparency avoids misconstructions and upholds trust.

13. How to Check a Valid Release of Settlement

Prior to your successful settlement bash, ensure that:

- The settlement letter includes both names (if joint).

- It consists of the account number and the exact balance settled.

- The text reads clearly:

“This loan is discharged wholly, and both borrowers are relieved of further responsibility.”

Without that language, the creditor may still pursue one party later.

14. If a Creditor Sues the Cosigner After a Settlement

Even if the collector/creditor actually files a lawsuit against the cosigner:

- Provide a written settlement agreement as a defence.

- Provide verification of payment for the full settled amount.

- Involve a debt lawyer now; they’ll be able to bring a motion to dismiss by way of prior release.

- if the collector continues to harass you.

In regard to proper documentation, courts are generally on the consumer’s side.

15. Do Creditors Require Cosigners to Consent to Settlement?

Creditors require cosigners to endorse a settlement if:

- The principal borrower is unable to repay fully.

- The creditor releases both parties with written confirmation.

- The financial gains outweigh the credit score losses.

Otherwise, it’s wiser to make regular payments to preserve credit.

16. How to Rebuild Credit After Settlement

Both borrower and cosigner are able to start to rebuild credit by:

- Paying all remaining accounts on time.

- Keeping your credit utilisation below 30%.

- Avoiding new debt temporarily.

- Like a secured credit card or credit-builder loan.

- Periodic verification of credit reports for discrepancies.

If your settlement is legitimate and final, your score will increment slowly over a period of 12–24 months.

Conclusion:

Debt settlement offers effective financial relief. However, adding cosigners or co-borrowers turns it into a group responsibility with shared repercussions. Credit score changes, legal responsibility, or taxes can impact anyone connected to the account.

Communication, transparency, and proper documentation provide you with the best protection. Before settling, be absolutely sure the creditor releases all parties in writing, and retain a copy of those documents for life.

That’s your guarantee that your journey to debt freedom won’t cause collateral damage to other people.

FAQs

[…] 12. Handling Multiple Settled Accounts […]