Overview

If you come to an arrangement to pay off part of a debt to an amount that is not the entire amount of the debt that is owing, then you should understand that the portion of the debt that is forgiven or canceled is not really going into thin air; it can literally be real income to the government. The Internal Revenue Service, or the IRS, views canceled debt as financial income or gain due to the fact that you have really received money, goods, or services without having to hold the burden of repaying the entire amount that you originally agreed to repay.

For instance, if you owed $10,000 and you paid off that amount with $6,000, the forgiven $4,000 is typically taxable. Most debtors find they receive a tax notice the second year after having paid off their debts. Familiarity with the rules of the IRS regarding forgiven debt will help prevent coming face-to-face with an unexpected expense.

Why Cancelled Debts Are Considered Taxable Income

The IRS regards forgiven debt as income due to:

- Money borrowed is not income while you owe to repay.

- If the amount to be repaid is forgiven by the money-lending company, then you’re actually better off than before.

- This “cancellation of debt income” (CODI) is taxable unless some exclusion or exception applies.

This fundamental principle is to hold that individuals should not be able to flee their duty of taxation by virtue of not facing their fiscal obligations.

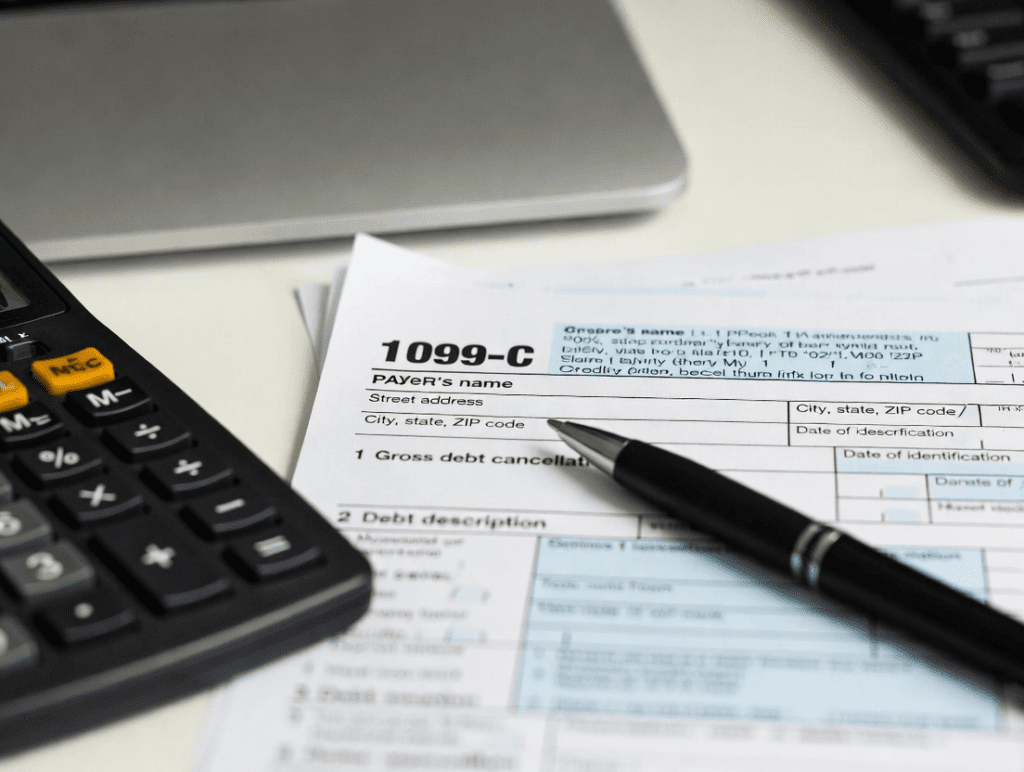

IRS Form 1099-C: Cancellation of Debt

What is Form 1099-C?

The lenders should provide Form 1099-C when they forgive $600 or more of debt. The form should also be filed with the IRS. The form discloses:

- Number of debts discharged.

- The day that the cancellation becomes effective.

- Information about the creditors.

The Reason Behind Its Importance

If Form 1099-C is received by you, the Internal Revenue Service will insist that on your return, you report as income the amount that was forgiven unless you qualify for an exclusion.

Example:

- You owe $15,000 against your card.

- Settle for $7,000.

- $8,000 is forgiven.

- The lender issues a 1099-C of $8,000 → You can be taxed on this money.

There is only a very limited category of qualified debt that is consistent with mortgages, and that is Qualified Principal Residence Indebtedness.

Exceptions to Taxable Forgiven Debt

Not all forgiven debt is reportable. There are excluded debts according to the rules of the IRS.

1. Exclusion of Insolvency

In this case of insolvency, wherein the amount of your debt exceeded the value of your assets during the time that the debt was forgiven, the Internal Revenue Service (IRS) offers a section that allows you to not have any canceled debt included in your taxable income.

- Example: Your liabilities were $20,000, and assets were $5,000. If you get a discharge of a $5,000 debt, you’re insolvent and can deduct it.

2. Bankruptcy Discharge

Debt forgiven during either Chapter 7 or Chapter 13 bankruptcy procedures is not considered taxable income to the individual. Bankruptcy’s legal protections ultimately supersede the tax laws of the IRS relating to forgiven debt.

3. limited category of qualified debt that is consistent with mortgages

The Mortgage Forgiveness Relief Act enables homeowners not to report forgiven debt on their main residence in case they qualify, including short sale or foreclosure.

4. Student Loan Forgiveness: Exceptional Rules and Regulations

In rare instances, such as with federal forgiveness programs such as the Public Service Loan Forgiveness (PSLF), forgiven student loans may not be subject to taxation. However, with private student loans, their forgiveness may still be taxed.

5. Types of Debts That Are Specifically Related to Business Operations and Farming

There exist rules and guidelines that pertain exclusively to business and farm-related debts that have been forgiven. Such personal debts can be excluded and not be taxed as income only if they can be directly connected with a case of financial hardship.

These debt forms were canceled and can possibly invoke a taxation burden:

- Credit Card Debts: Most commonly settled and reportable if forgiven.

- Personal Loans: If a personal lender foregoes the payment requirement, remember that this forgiveness can potentially be considered taxable income.

- Forgiven medical bills by the hospital or through collections can be construed to be income that is taxable.

- Mortgage Debt: Taxable unless qualified for exclusion.

- Auto Loans: If repossessed and any amount forgiven is included in the balance, the forgiven amount can be subject to taxation.

How to Report Cancelled Debt on Your Tax Form

Step 1: Receive Form 1099-C

The creditor must distribute it by not later than January 31 during the year following the cancellation.

Step 2: Seek Out Exclusions

First, find out whether you qualify for the conditions of insolvency, bankruptcy, or any other exemptions that may be provided by the IRS.

Step 3: Fill Out Form 982 of the IRS

Schedule 982, known officially as “Reduction of Tax Attributes Due to Discharge of Indebtedness,” plays the valuable role of being filed to properly report various exclusions that can come into play with unique financial scenarios.

Step 4: File a Detailed Report of the Tax Return

If you’re not excluded from this requirement, then you’ll report the amount forgiven as “Other Income” on your Form 1040.

Illustrative Examples Concerning the Tax Implications Surrounding Cancelled Debt

Example 1: Settling Credit Card Debts

- Debt: $12,000

- Settlement amount determined: $6,000.

- Forgiven amount: $6,000.

- Reportable Income: $6,000 (unless insolvent).

Example 2: A Short Sale Mortgage Transaction

- Mortgage: $200,000

- Home sold for $160,000

- Forgiven amount: $40,000.

Excluded from the scope of review if it falls within the conditions set by the rules of mortgage relief.

Example 3: The Bankruptcy Discharge of Debts

- Debt: $25,000

- Filed in Chapter 7 Bankruptcy

- Reportable Income: $0 (excluded)

How Insolvency Relates to Forgiven Debt

The Internal Revenue Service refers to insolvency as a precise financial situation where the total dollar amount of your debts that you owe is greater than the fair market value of all of the assets that you really possess.

For instance,

- Total debt: The amount of $50,000.

- Total Assets: $30,000

- Insolvency Amount: $20,000

- If a debt of $10,000 is forgiven, then that amount is completely exempted out of your income to be taxed because you were insolvent to the extent of $20,000.

The debtors are required to submit and return Form 982 and submit detailed documentation explaining their assets and their liabilities.

Similar Rules Detailed by the IRS Regarding Mortgage Forgiveness

The Mortgage Forgiveness Debt Relief Act, which had been extended periodically over the years, provides a very useful privilege that enables qualified taxpayers to exclude debt that is forgiven on their primary home. But again, special rules and standards must be abided by to be qualified:

- Must be the primary residence.

- Forgiveness must be due to foreclosure, short sale, or loan restructuring.

- Restrictions apply to the highest amount that is not capitalized.

IRS Provisions Concerning Student Loan Forgiveness

- Federal Student Loan Forgiveness Policies: loans forgiven by having qualified for PSLF, income-driven repayment, or by death or disability discharges may be exempted from income taxation (by recent guidance of the IRS).

- Private Student Loans: They are not canceled and thus not exempt. But canceled debt is not subject to tax unless there is insolvency or bankruptcy.

Effects of Failure to Report Cancelled Debts

Neglecting to report any forgiven debt that is taxable can have several potential effects, including:

- IRS penalties.

- Interest on unpaid taxes.

- An audit or legal consequences.

Although you may have the assumption that you are qualified to be exempted, you will need to take the proper steps to fill out the correct forms to prevent any future disputes with the IRS.

Techniques Applied to Reduce Tax Liability of Cancelled Debts

- Claim of Insolvency: If qualified, use Form 982 of the IRS.

- File Bankruptcy (Final Option): Bankruptcy debt is exempt from taxation.

- Investigate and compare the various mechanisms of debt relief applicable to mortgages, particularly if the case is regarding your primary residence.

- Consult a Tax Professional: Tax law is extremely complex, and professional advice prevents us from making mistakes.

Conclusion: Acquiring an Overall Perspective of the Tax

Debt settlement can be a welcome relief, but forgiven debt sometimes results in taxation. The canceled debt is considered income by the IRS unless you’re exempt by insolvency, bankruptcy, or special relief acts. Always keep an eye out for the Form 1099-C of the IRS, re-evaluate your financial situation, and file the appropriate forms.

By getting involved with the appropriate and prudent planning, you can effectively handle debt that is forgiven without being blindsided by any surprise tax bills that could make life tougher financially.

Informing yourself of the rules and regulations of the IRS will allow you to make shrewd and prudent financial decisions and eventually escape any unpleasant surprises that can occur during that notoriously stressful period of the year, tax season.

FAQS

No. Forgiven debt can be exempted if you were insolvent, filed bankruptcy, or qualify through special programs, such as the Mortgage or Student Loan Forgiveness.

It is a cancellation of debt from creditors when they forgive $600 or more of debt. The IRS also receives a copy.

Yes. There is no taxation of discharged bankruptcy debt.

You will need to properly calculate and identify your debts over assets on the very date of forgiveness, and through this computation, you will have to provide the IRS with Form 982.

Some of the federal programs don’t provide tax forgiveness of loans, but forgiveness of private loans is usually taxable.