An Overview of Debt Settlement

Debt settlement while in collection is a process by which a consumer negotiates with a debt collector or with a debtor’s original creditor to settle the debt by agreeing to make payment of an amount that is less than the full amount of debt. When an account enters into delinquency and then into the collection process, the debtor’s original creditor will sometimes deem that they can better collect money by taking a portion of the debt rather than losing the full amount. As a consumer, this can provide an opening to settle financial debt without having to go through bankruptcy procedures. Bankruptcy can be a long and overwhelming experience, and being aware of this can make debt settlement an appealing option. But debt settlement is not without repercussions, and these risks need to be clearly known and seriously thought about before any debt settlement motives are undertaken.

This is the comprehensive piece about debt settlement while being collected on by creditors, covering the process, negotiating tactics, legal rights and responsibilities, pros and cons, taxation, and advice on handling finances after settlement.

Getting to Know the Process of Debt

What Is Debt Collection?

Debt collection is the process of pursuing payment against overdue accounts. When you miss a few payments on credit cards, loans, or any financial debt, your creditor will either send out their internal collections department or will sell the account to an external third-party collection firm.

Operations of Collection Agencies

Collection agencies will normally practice buying or handling accounts way below the actual cost, their only goal being to collect as much money as possible from these debts. Let’s take an example of a situation where you owe an amount of $10,000. A collection company may have purchased your debt for an amount of only $2,500. That’s exactly why they will be willing to settle on an amount that is way below the actual amount owed.

Original Creditor versus Collection Agency

- Original Creditor refers to the bank or financial institution itself that you borrowed money or took the initial loan from.

- Collection agency: A business that buys your debt or collects on behalf of the creditor.

Recognition of the identity of the person or entity that owes the money is crucial, as this will greatly determine the approach that you will employ during negotiations.

How the Process of Debt Settlement Collections Works

Debt settlement with accounts in collections entails coming up with a payment of an amount or establishing a payment plan to close and settle the account.

Negotiating with Credit Bureaus

Either you or a qualified negotiator can call the collector with the purpose of offering a settlement amount that is less than the original amount. Here, keep in mind that many times collectors are willing to settle this kind of offer, because receiving a portion of the debt that is being owed is better than receiving nothing.

Payment of a Lump-Sum Compared to a Payment Plan

- Lump-Sum Payment: The payment of one agreed amount, typically between 30 to 60% of the balance

- Payment Plan: Payment over multiple payments. Not very productive due to the preference of the collectors to be paid in cash.

Usually Noted Settlement Percentages

Most settlements will be between the 40 to 60% of the original debt, but this will depend on the type of debt, the policies of the creditors, and your unique financial situation.

The Good and Bad of Entering into Debt Settlements During Collections

Benefits of Debt Settlement

- Lowered Balance: There is a chance that you can make a payment that will be way short of fifty percent of the amount that you already owe.

- Avoiding Legal Litigation: Being proactive to solve issues at an early stage can greatly help minimize the chance of litigating against you by your creditors.

- Financial Relief: Relieves you of crushing debt and allows attention to building.

Potential risks of debt settlements

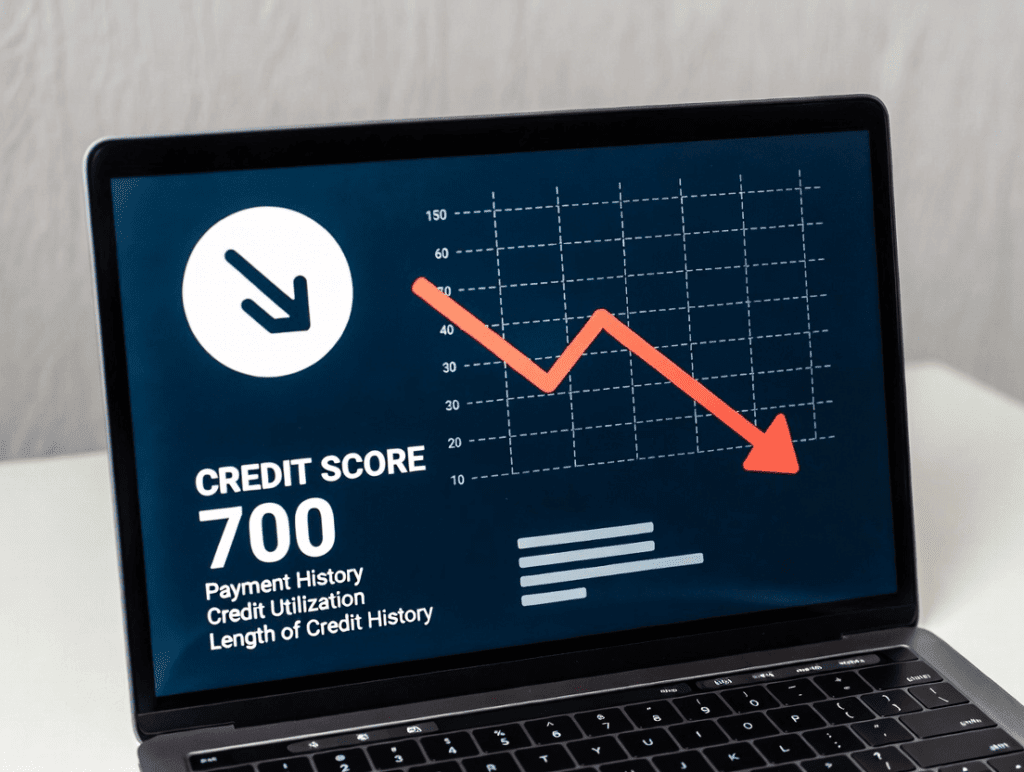

- Credit Score Harm: When you settle, it can be listed as “settled for less than full amount,” which can harm your credit score adversely and therefore reduce it considerably.

- Tax Consequences: The forgiven amount may be treated as taxable income.

- Upfront Payments: The collectors typically prefer to receive money in lumps, which is not always easy to mobilize.

Strategies for Negotiating Debt Settlement During the Collections Process

1 Know Your Budget Limits:

Review and determine the amount that you can afford to spend without causing any strain on your finances.

2 Negotiate As If There’s No Tomorrow:

BEGIN LOW. Negotiating is a numbers game, and you can always decrease.

3 Request a Written Settlement Agreement:

Do not ever send money without first getting a proper written agreement.

4 Do Not Give Access to Bank Account:

Pay by cashier’s check or third-party.

5 Finding the Ideal Time for Your Negotiation:

- Before charge-off (within 180 days of delinquency) → Creditors will be more forgiving.

- After charge-off → agencies may settle for lesser amounts.

Debt Settlement vs Debt Consolidation vs Bankruptcy

Debt Settlement

- Negotiates down the amount.

- This plan is suited best to individuals who owe a large sum of money but have some payment potential.

Debt Consolidation

- Brings together various outstanding debts into a single loan that comes with a reduced interest rate.

- Helps to organize and run payments; however, adds nothing to decreasing the overall sum balance.

Bankruptcy

- Legal procedure to relieve debt.

- Extremely adverse credit effect, but provides a new beginning.

Which one is appropriate for you?

- If you can afford to pay part of → settlement.

- If you want to make payments lower → consolidation.

- If you’re drowning with no income → bankruptcy.

Legal Rights During Debt Collection Settlement

The Fair Debt Collection Practices Act, or the FDCPA, is an important legal protection that exists to help consumers residing within the United States.

Collectors Are Unable

- Harass or threaten you.

- Calling after 9 p.m. or before 8 a.m. without permission.

- Falsely claim a different total regarding the amount that is owed.

You have the inherent right to:

- I respectfully request a written confirmation of the debt.

- Challenge illegitimate or outdated debts.

- Halt all communications requests except legal notices.

- Knowledge of rights allows you to negotiate boldly.

Effect of Credit Card Debt Settlement During Collections

The debt settlement will lower your credit score, but by how much varies:

- Short-Term Effect: Credit rating falls due to the account reflecting “settled for less than full balance.”

- Long-Term Impact: As time passes and you rebuild with responsible credit use, the effect lessens.

The settlement will remain on your credit report normally for seven years, and this begins with the date of the first delinquency.

Tax Implications of Debts Settled during Collections

If a creditor cancels debt of more than $600, he or she will be required to provide you and the Internal Revenue Service with a Form 1099-C.

- Forgiven debt is regarded as taxable income.

- Example: If you settle a $10,000 debt with $5,000, then the $5,000 forgiven can be considered taxable.

- There are exceptions to insolvency (in which your debts outweigh assets).

It is always best to ask the advice of a tax advisor before you go to settle any sort of agreement.

When to consider Professional Debt Settlement Companies?

Debt settlement companies will negotiate with companies on your behalf, but be wary.

How They Work

- Each month, you always contribute a set amount of money to a different savings account.

- When enough money is accumulated, the company negotiates settlements.

Warning Signs of Bogus Schemes

- Payment in advance of services.

- Certain results are assured.

- Urging you intensely to discontinue payments to your debt-holders.

DIY or Professional Help

- DIY Settlement: It costs nothing to settle this way, but you will require assertiveness and bargaining skills.

- Professional Assistance: Convenient to have if you’re busy, but always research their reputation.

Guidelines to Prevent Future Collections After Reaching a Settlement

- Create a Budget: It is very important to keep a very close track of money that’s being received and money that’s being spent to effectively manage and keep track of all of your bills.

- Saving through an Emergency Fund is of key importance: having just enough savings to your name can provide an important item of insurance against unforeseen expenses that will inevitably arise sooner or later.

- Use Credit Smart: Manage Credit Wisely: Pay your balance down and make payments before the due date.

- Validate Credit Reports: One should ensure that paid-off accounts actually show up on the report.

Conclusion: Dealing with Debt Settlement During Collection

Debt settlement, while being collected on, can actually be an effective and helpful option for consumers who are facing large amounts of debt. This process allows you to negotiate and settle your financial responsibilities by paying less than the amount you owe, but keep in mind that this choice is not without some negatives, including possible harm to your credit rating and potential taxation.

Prior to coming to the decision to settle, being an option, you should compare this with other options, including consolidation or bankruptcy. You should also learn about your rights here and invest the necessary amount of time assessing your future financial outlook to make the best decision for your situation.

Debt settlement provides comfort and a way out of financial instability for those who handle it responsibly.

Frequently Asked Questions (FAQs)

Usually, between 40 to 60% of the original debt, depending on settlements.

Indeed, after a legally binding agreement is achieved through writing and the payment is conducted with success, all efforts to collect should cease promptly.

The period of time may extend to seven years, dating back to the origin of the first delinquency.

Indeed, there exists a considerable number of individuals able to negotiate with collection agencies by and large.

Indeed, debt that was canceled and exceeded $600 is many times taxable, excluding exemptions.