Overview of the Errors That Can Be Made in Credit Report Settlements

The credit report is key to understanding an individual’s financial health. Banks, lenders, and landlords use it to assess your creditworthiness, which influences their decisions. Once a loan is paid off or a credit card balance is cleared, your credit report needs to reflect this positive outcome. Unfortunately, many people find errors and inconsistencies on their credit reports after making these payments. These mistakes can hurt your credit score, making it harder to secure new loans or credit cards in the future.

This complete guide seeks not only to fully explain why errors appear after the settlement but also how those errors can harm your credit rating. It outlines the specific steps you need to take to successfully remove them from your report.

What Are the Reasons That Errors Get on Credit Reports after Resolution?

There could be reasons why mistakes could appear on your credit report despite the fact that you paid the repayment dues fully and completely:

- Slow Updates: In some cases, the lenders will take months or even weeks at times before reporting updated details to the credit bureau.

- Clerical Errors: Errors caused by human intervention during the entry of data may frequently lead to the display of the wrong details of an account.

- Duplicate Reporting: It may so happen that the same account gets reported twice; on the first reporting, it might be reported as ‘unpaid’, and on the second reporting, it may appear as ‘settled’.

- Technical Faults: Automatic programs could erroneously identify accounts as open or overdue as a result of faults, leading to the inappropriate determination of the account.

Miscommunication occurs when the lender doesn’t provide the correct settlement details to the credit bureaus, leading to discrepancies.

Types of errors occur when credit reporting

The settlement mistakes may occur in different guises. Hereafter is the list of the most common types encountered:

1. The status of the accounts is not correct

Even after the settlement has been affected, the account might still reflect as “open” or “active” rather than being indicated as “settled” or “closed”.

2. Cases of Duplicate Entries

Occasionally, the same account appears twice on the list – once as being unpaid, then as being settled. That lowers your credit score unnecessarily.

3. Failure to Achieve Correct Financial Ratio after the Settlement

The report may also reflect an extra payment for an outstanding balance when you have actually paid the settlement amount.

4. Settled but Still Marked as “Unpaid.”

Credit bureaus may also not indicate the account on their records as being paid, but as being unpaid, thereby severely hampering creditworthiness.

5. Late Payment Errors after the Settlement

Even after you pay off your account successfully, there might still be marks on your account for late payments.

The Effect of Mistakes on Your Credit Report and How It Affects You

Errors committed after the settlement process could significantly impact your credit report negatively:

- Lower Credit Score: Errors on the report could lower the score by 50-100 points.

- Refusal of Loans: There could well be the risk of banks refraining from sanctioning any future applications for credit cards or loans.

- High Rates of Interest: There may also be the risk of paying higher rates of interest even when you obtain approval.

- Loss of Trust: Due to certain reasons, the lenders might get the impression of you as being a high-risk borrower.

Thus, it becomes extremely vital to eliminate and correct them at an early stage for the purpose of continuing and ensuring fiscal stability.

Accurate Stepwise Guide for the Procedure for Correcting Settlement Errors

The following outlines an exhaustive and clear step-by-step process you can use in order to properly identify and fix any potential mistakes appearing on credit reports after settlement has been achieved:

1: Read your credit report carefully.

- You can obtain a free credit report for the three large credit bureaus, which include Experian, Equifax, and TransUnion.

- Confirm all the information: the settlement numbers, balances, settlement status, and payment history.

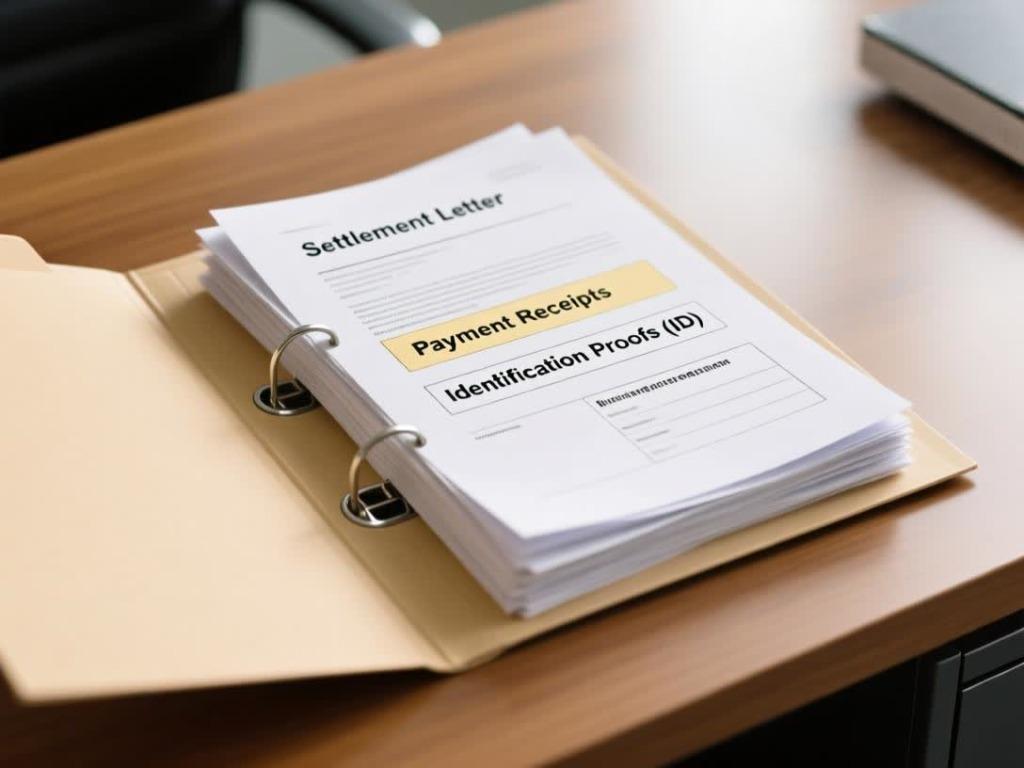

2: Assemble the Required Supporting Documents

- It is advisable to retain the settlement letter issued by the lender.

- Bring bank receipts or payment evidence.

- Retain emails or letters from creditors indicating settlement.

3: Open and Register a Formal Dispute at the Credit Bureaus

- Call the credit bureaus personally (internet, mail, or phone).

- Bring us photocopies of valuable documents.

- Clearly indicate the nature of the error as well as the correct correction.

4: Approach the Lender or Creditor Directly

- Be sure to let them know about the reporting error made.

- Please make a request to them, asking that they send the corrected information directly to the bureau for processing.

- In some cases, the verification process with the creditors can greatly speed up the correcting process.

5: Continue Following up until the Required Correction is Completed Fully

- It takes 30–45 days on average for bureaus.

- If not corrected, escalate the issue with more supporting documents.

- Express all communications for the purpose of legal evidence.

How long does it take on average to rectify errors after a settlement has been reached?

The time varies according to the credit bureau as well as the lender:

- First Investigation: 30 days (in exceptional cases, 45 days).

- Corrections Update: 1–2 billing cycles.

- Complete Resolution: Usually 1–3 months.

Patience is necessary, but the follow-up gets the quick results.

Common Mistakes People Make During the Dispute Process

Everybody procrastinates or handles conflicts ineptly, so mistakes persist. Do not make the following mistakes:

- Not ensuring the safe storage and security of settlement documents.

- Filing false claims without supporting evidence.

- Only reaching the bureau, but not the lender.

- The first complaint was not followed up.

- Expecting an instant result.

Protected Rights: How the Fair Credit Reporting Act Is Compatible with the Bill of Rights

The Fair Credit Reporting Act (FCRA) in the United States protects consumers who might be wrongfully reported. FCRA states as follows:

- You have the right to dispute inaccurate information.

- The credit bureaus should carry out the right investigation within 30 days at the latest.

- Erroneous entries must be corrected or struck.

- You may obtain the right for free once annually to get a copy of your credit report.

- In the case of mistakes not being rectified, you may bring the matter before the courts.

Knowing exactly where you stand regarding rights affords you a stronger and fortified power to oversee and control your financial information.

Means of Effectively Avoiding Errors in the Event of Future Settlements

Prevention is the best cure. Apply the next tips:

- It is also best to require a written settlement letter from the lender.

- Payment settlement using trackable channels (bank transfer, check, etc.).

- Follow up with the lender after settlement for verification of reporting.

- It’s best to review your credit report at least twice per year.

- Challenge errors on the spot instead of later.

Knowing when it’s the Best Time for Professional intervention

In the event errors are not rectified after numerous disagreements, then consider:

- Credit Repair Agencies – It resolves conflicts on your behalf as needed (but choose only licensed agencies).

- Consumer Protection Lawyers – In situations where lenders or bureaus deny reasonable adjustments.

- Financial Advisors – To counsel you on how best you can reconstruct your score after settlement.

Conclusion:

Having a Clean and Up-to-Date Credit Report Errors on your credit report after correcting them are not just a frequent event but also fully rectifiable through the appropriate procedures and due process. Such mistakes could significantly negatively affect the credit rating of an individual, limit the financial future of an individual, and introduce unnecessary degrees of stress that might permeate the entirety of the remaining life of an individual.

Taking the time to diligently go through your credit report, procuring the relevant evidence of any errors, submitting disputes where necessary, and being educated about your constitutional rights may help you effectively eliminate these mistakes from the report.

It is always best to also be proactive about it and develop the habit of checking your credit frequently so you get to keep a healthy, positive credit profile.